Health care costs continue to rise, making it more important than ever to understand the tools available to manage out-of-pocket expenses. Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs) allow individuals and families to pay for qualified medical expenses using pretax dollars, helping reduce the overall cost of care.

With family health insurance premiums up nearly 300% since 2000 and now averaging more than $25,000 annually, many employees feel the squeeze. Deductibles have also climbed meaningfully over time, increasing out-of-pocket exposure. Understanding — and using — HSAs and FSAs can help families take greater control of their health care finances.

What Are HSAs and FSAs?

HSAs and FSAs are tax-advantaged accounts designed to help manage medical expenses.

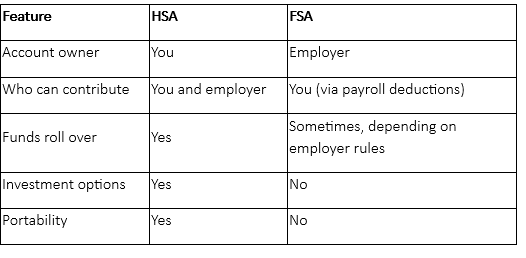

A Health Savings Account (HSA) is available to individuals enrolled in a high-deductible health plan (HDHP). Contributions can be made by you and, in some cases, your employer. Unused funds roll over from year to year and remain yours even if you change jobs or retire.

A Flexible Spending Account (FSA) is typically employer-sponsored and funded through pretax payroll deductions. Unlike HSAs, FSA funds generally must be used within the plan year, unless your employer offers a grace period or limited rollover.

Both accounts can be used to pay for qualified medical expenses — such as copays, prescriptions, and certain over-the-counter items — with pretax dollars. Which account makes more sense depends on your health plan, expected medical costs, and broader financial picture.

Key Differences Between HSAs and FSAs

2026 Contribution Limits

For 2026, the IRS allows individuals to contribute up to $4,400 and families up to $8,750 to an HSA. Individuals age 55 or older may contribute an additional $1,000 annually as a catch-up amount.

The health care FSA contribution limit for 2026 is $3,400. Employers that permit carryovers may allow up to $680 of unused FSA balances to roll into the following plan year.

Why HSAs and FSAs Matter More Than Ever

Rising premiums and deductibles mean households are absorbing a larger share of health care costs than in the past. In many cases, it now takes several weeks of full-time work just to cover the employee portion of annual premiums — before accounting for any medical care.

Employers are also shifting costs through narrower provider networks, increased prior-authorization requirements, and tiered drug pricing. HSAs and FSAs help offset these trends by allowing families to set aside pretax dollars for both expected and unexpected medical expenses.

If HSA funds are used for non-qualified expenses before age 65, ordinary income taxes and a 20% penalty generally apply. After age 65, non-qualified withdrawals are taxed as ordinary income, but no penalty applies. While HSA contributions are exempt from federal income tax, some states may tax contributions.

Real-Life Situations Where HSAs and FSAs Can Help

Growing Families

Having a baby often brings higher medical costs, including prenatal care, delivery, and pediatric visits. An FSA can help cover short-term expenses, while an HSA allows unused funds to be carried forward for future medical needs.

Career Changes

Changing employers may involve moving to a high-deductible health plan. An HSA remains yours even if you change jobs or retire, making it a flexible long-term planning tool.

Chronic Health Conditions

Ongoing copays, prescriptions, and specialist care can add up over time. HSAs and FSAs can help manage these recurring medical expenses more efficiently.

Caring for Aging Parents

Medical and caregiving-related costs often increase as parents age. These accounts may help families manage the financial impact of elder care.

Practical Tips

- Estimate anticipated medical expenses before making annual elections

- Monitor balances and eligible expenses throughout the year

- If you have an HSA, review available investment options

- Revisit benefits during qualifying life events such as marriage, birth, or job changes

Final Thoughts

HSAs and FSAs can play an important role in managing rising health care costs when used thoughtfully and in coordination with a broader financial plan. Understanding the trade-offs between these accounts can help support both short-term savings needs and longer-term financial flexibility.

This content is provided for general informational purposes only and should not be considered tax or legal advice. Please consult qualified tax or legal professionals regarding your individual situation.