The first quarter of 2026 was dominated by a sharp escalation in geopolitical risk, which became a central driver of global market volatility in the second half of the quarter. Tensions intensified early in the year following tariff-related policy developments, followed by a rapid deterioration in Middle East stability after joint US and Israeli military actions against Iran in late February. These events unsettled financial markets, disrupted energy supply expectations, and contributed to elevated oil prices and inflation concerns worldwide. While diplomatic developments and shifting headlines fueled abrupt market swings throughout the quarter, they also served as a reminder of how quickly global events can influence investor sentiment.

Global equity markets declined during the first quarter, with U.S. stocks underperforming both international developed and emerging market peers. Value stocks outperformed growth stocks across most regions, and small-cap stocks generally fared better than large-cap. Real estate investment trusts (REITs) were a relative bright spot, with U.S. REITs outperforming broader equity markets during the quarter. On the last day of the quarter, major indices rebounded with hopes that the conflict in the Middle East would soon come to a close.

Given the heightened market volatility, the Federal Open Market Committee decided to hold its key interest rate steady between 3.5-3.75% during its March meeting and made few changes to its view on the economy. Additionally, jobs reports fluctuated throughout the quarter. January had strong additions, February showed an unexpected downturn, and March rebounded with an addition of 178,000 nonfarm payroll jobs.

Housing market conditions during the first quarter of 2026 remained constrained, with affordability pressures continuing to weigh on buyer activity amid elevated and volatile mortgage rates. The average 30‑year fixed‑rate mortgage fluctuated meaningfully throughout the quarter, briefly dipping below the 6% level for the first time since 2022 before moving higher again by late March.

Oil prices surged sharply, with crude oil surpassing $100 per barrel in early March for the first time since 2022, driven by concerns over supply disruptions stemming from the Middle East conflict. The International Energy Agency announced plans for the largest release of emergency stockpiles of global strategic reserves in the IEA’s history in response to rising prices and geopolitical risk. These developments contributed to elevated gasoline prices in the U.S., which moved above $4 per gallon by the end of March, up roughly 35% from the end of 2025. The strength in oil prices supported energy‑related assets and contributed to broader inflationary pressures during the quarter.

FIRST QUARTER EQUITY INDEX RETURNS

Although global markets faced a notable downturn during the middle of the quarter, solid gains earlier in the period helped offset those declines, resulting in global equity indices finishing the quarter mixed, from modestly negative to modestly positive. Small cap and value stocks across the globe outperformed their large, growth-oriented counterparts.

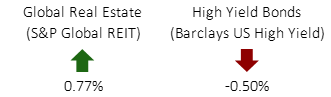

FIRST QUARTER ALTERNATIVE INDEX RETURNS

US REITs were among the strongest asset classes for the quarter, returning over 4.5%. However, non-US REITS suffered, losing nearly 8%. Despite the negative performance of non-US REITs, the global REIT index, more heavily weighted towards US REITs, had a modestly positive return. High yield bonds struggled modestly.

FIRST QUARTER FIXED INCOME INDEX RETURNS

Yield curves in the US, and largely across the globe, rose over the quarter. The headwinds caused a modestly negative return for the US Aggregate Bond Index. TIPS and municipal bonds had positive returns.

The strong start to the year led to better returns for the quarter than financial headlines might have suggested. The economy remains in a strong condition, and we are optimistic that markets will attain new highs after the war in the Middle East subsides.

As always, we look forward to working with you throughout the year and welcome calls with questions or concerns.